"Demystifying and straight talking"

- Sarah Haller, Property Solicitor -

Andrew Boast FMAAT

- Book Author -

Andrew is the Co-Founder of SAM Conveyancing and a qualified accountant. In a career spanning more than 22 years he has guided thousands of clients through the complex process of buying a home. He has written and consulted extensively on the property market and this is his second book.

How much deposit do I need to buy a house?

"For most mortgage lenders, you’ll need a minimum of a 10% deposit. Buy to let landlords will require a minimum of 25%. The best mortgage interest rates are where you can invest 40% or more deposit. But, as a first-time buyer, it’ll take years to save up 40% without a gift from friends or family."

Generally, you will be asked for a deposit of 10%. 5% deposit mortgage products are much harder to come by since the affordability crisis of 2022. New schemes have been introduced to make it easier to buy a house without killing anyone. Options include Save to Buy, which allows buyers to make a purchase with just a 1% deposit or Rent to Buy.

There are some alternate options for buying a house with no deposit. Chapters 1 to 2 guide you through saving a big enough deposit to buy a house and how to make a winning offer. Whether you've found a property, or are just in the early stages, this book has insight to help you.

Prev

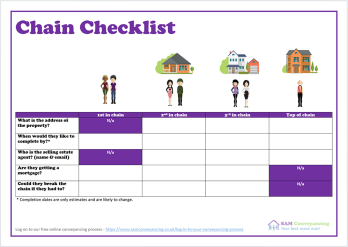

Use the interactive checklist - Managing The Property Chain

Why does buying a house make you want to kill someone? · Who are the players in the game? · Is a mortgage valuation a defect survey? · What is a chain? · Why does it take so long? · What are the different types of affordable housing?

Available on Amazon | Kindle | Paperback

Use the interactive table guide - Market Research & our online tool - How To Make An Offer On A House

What can you afford? · How to save a ‘big enough’ deposit · How to find a property to buy · How do you make a Winning Offer? · What if they don’t accept your offer? · What happens if the bank undervalues the property?

Available on Amazon | Kindle | Paperback

Do I have to use a solicitor? · Should I use a solicitor or a conveyancer – what’s the difference? · How do I choose the best conveyancing solicitor? · What are the costs of buying a house? · What happens after I instruct a solicitor?

Available on Amazon | Kindle | Paperback

Overview of the mortgage process · How to get a mortgage · Should I secure a fixed rate for 2 or 5 years? · Should I secure a mortgage for 25, 30, 35 or 40 years? · What do you do once you get a mortgage offer? · How do you sign a mortgage deed? · Can a mortgage offer be rescinded?

Available on Amazon | Kindle | Paperback

What are the different types of surveys? · How much do property defects cost to fix? · How do I renegotiate?

Available on Amazon | Kindle | Paperback

What are conveyancing searches? · When should I order my searches? · How long do searches take to come back? · I need to exchange but I don’t have my local authority search back - What can I do? · Which searches are mandatory for my mortgage lender? · I’m a cash buyer, do I need searches?

Available on Amazon | Kindle | Paperback

What are draft contracts? · What are enquiries? · What enquiries are deal breakers? · No reply, get indemnity insurance? · What are reasonable times to wait for stuff to get done? · What is the most efficient way to get an update? · How do you protect yourself when buying with someone else?

Available on Amazon | Kindle | Paperback

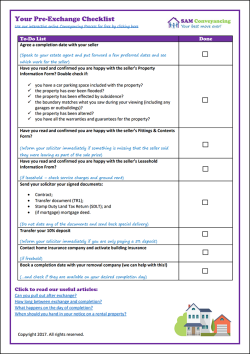

Use the interactive checklist - Exchange Of Contracts

What do I need to sign? · What happens if the purchase falls through? · What is exchange of contracts? · What happens if I pull out after exchange? · How long between exchange and completion? · Can I get access between exchange and completion? · Hire a van or get removals? · When should you walk away from the purchase?

Available on Amazon | Kindle | Paperback

Use the interactive checklist - Completion Day

What happens the day before completion? · What happens on completion day? · What can cause a delay? · What happens if you complete the next working day? · Seller has left junk in the garage, what can I do?

Available on Amazon | Kindle | Paperback

Use the interactive checklist - First Day In Your Home

Day 1 in your own home · What does my solicitor do after completion? · Neighbours, everybody needs good neighbours! · What happens next? · What happens if I can’t afford to repay my mortgage?

Available on Amazon | Kindle | Paperback

Next

Chapter 1

The Conveyancing Process Explained

Use the interactive checklist - Managing The Property Chain

Why does buying a house make you want to kill someone? · Who are the players in the game? · Is a mortgage valuation a defect survey? · What is a chain? · Why does it take so long? · What are the different types of affordable housing?

Available on Amazon | Kindle | Paperback

Chapter 2

How To Get Your Offer Accepted

Use the interactive table guide - Market Research & our online tool - How To Make An Offer On A House

What can you afford? · How to save a ‘big enough’ deposit · How to find a property to buy · How do you make a Winning Offer? · What if they don’t accept your offer? · What happens if the bank undervalues the property?

Available on Amazon | Kindle | Paperback

Chapter 3

Instruct A Solicitor

Do I have to use a solicitor? · Should I use a solicitor or a conveyancer – what’s the difference? · How do I choose the best conveyancing solicitor? · What are the costs of buying a house? · What happens after I instruct a solicitor?

Available on Amazon | Kindle | Paperback

Chapter 4

How Are You Financing The Purchase?

Overview of the mortgage process · How to get a mortgage · Should I secure a fixed rate for 2 or 5 years? · Should I secure a mortgage for 25, 30, 35 or 40 years? · What do you do once you get a mortgage offer? · How do you sign a mortgage deed? · Can a mortgage offer be rescinded?

Available on Amazon | Kindle | Paperback

Chapter 5

Are There Any Defects with My Property?

What are the different types of surveys? · How much do property defects cost to fix? · How do I renegotiate?

Available on Amazon | Kindle | Paperback

Chapter 6

Conveyancing Searches

What are conveyancing searches? · When should I order my searches? · How long do searches take to come back? · I need to exchange but I don’t have my local authority search back - What can I do? · Which searches are mandatory for my mortgage lender? · I’m a cash buyer, do I need searches?

Available on Amazon | Kindle | Paperback

Chapter 7

Contracts And Enquiries

What are draft contracts? · What are enquiries? · What enquiries are deal breakers? · No reply, get indemnity insurance? · What are reasonable times to wait for stuff to get done? · What is the most efficient way to get an update? · How do you protect yourself when buying with someone else?

Available on Amazon | Kindle | Paperback

Chapter 8

Exchange Of Contracts

Use the interactive checklist - Exchange Of Contracts

What do I need to sign? · What happens if the purchase falls through? · What is exchange of contracts? · What happens if I pull out after exchange? · How long between exchange and completion? · Can I get access between exchange and completion? · Hire a van or get removals? · When should you walk away from the purchase?

Available on Amazon | Kindle | Paperback

Chapter 9

The Day Of Completion

Use the interactive checklist - Completion Day

What happens the day before completion? · What happens on completion day? · What can cause a delay? · What happens if you complete the next working day? · Seller has left junk in the garage, what can I do?

Available on Amazon | Kindle | Paperback

Chapter 10

You're No Longer A First-Time Buyer, Now What?

Use the interactive checklist - First Day In Your Home

Day 1 in your own home · What does my solicitor do after completion? · Neighbours, everybody needs good neighbours! · What happens next? · What happens if I can’t afford to repay my mortgage?

Available on Amazon | Kindle | Paperback

1. Work out how much you can afford to spend

You'll need to save up a deposit, you might be lucky enough to get some help towards your deposit with a gift from your parents. You'll need a mortgage illustration from your lender to show how much they might be willing to lend you (this stage of the mortgage application process is not credit checked).

Chapter two of the book includes calculations for working out your maximum budget.

2. Find a house and make a winning offer

House hunting is the fun bit, but it can be heart breaking to find your dream home and have your offer rejected. Chapter 2 includes tips for finding your house, and our tried and tested formula for getting your offer accepted.

3. Instruct a Solicitor

This can actually be done before you make your offer, which may help you get it accepted. Having a communicative solicitor makes every difference to your home buying experience which is why at SAM we assign you a dedicated conveyancing executive to case handle your purchase. Chapter 3 contains all you need to know when choosing a solicitor and what you'll need to provide them with to get things underway.

4. Apply for your mortgage (the lender will value the property)

A mortgage broker is so helpful when choosing the right product and making your application, Chapter 4 covers tips on improving your credit score and submitting your application.

The lender will have a valuation conducted to be sure that the property is worth the money they are lending, Chapter 2 includes a section explaining what you can do if the lender undervalues the property.

5. Conduct Surveys & Searches

We would never recommend anyone buy a house without having a survey. You'll need to choose between a Level 2 or Level 3 survey, (unless it a new build, in which case you'll want a snagging survey) our team will happily talk you through these options. Your conveyancing searches are normally ordered by your solicitor on your behalf. Your SAM Conveyancing quote will include the standard search bundle. Your solicitor will recommend any additional searches appropriate for your specific property.

6. Your solicitor conducts legal enquiries

The seller's solicitor sends over a draft contract pack for your solicitor to review. Your solicitor reviews all of the documents for any legal concerns and then raises enquires that the seller and their solicitor must answer. In order to complete their legal enquiries, your solicitor will also need your ID/Proof of Funds/Formal instruction documents, Mortgage Offer, Property Searches and Survey (if ordered).

If your solicitor finds there are defects with the property or queries which can't be resolved, they can help you negotiate a better price with the seller. In some cases it may be advisable to pull out of the sale all together.

7. Exchange Contracts

When the terms of the purchase have been agreed, you and the seller sign the contracts, legally binding you to complete the transaction (if you don't there are penalties). You'll also sign the TR1 Transfer Form, Stamp Duty Land Tax Form (SDLT) & Mortgage deed (if applicable). You will now be responsible for insuring the building (unless you're buying a leasehold).

8. Completion

To make sure you complete on time, it can help to transfer your completion monies the day before. your solicitor collects your mortgage funds (if you're using one) and your completion monies, then sends the full purchase amount to the seller's solicitor. Then the sellers solicitor release's the keys and you can collect them from the estate agent. Make sure you get all your keys, check the property is empty, check the meter readings and inform the utilities company(ies) of the change of ownership.

9. Post Completion.

Time to move in! Your solicitor files your Stamp Duty Land Tax form and pays any tax due. If the property is leasehold, they will obtain notice from the freeholder or their management agent. Finally they'll make an application to register your ownership at the Land Registry.

How to Buy a House without killing anyone looks into each of these stages in depth, with tips and guidance along the way, for handling all of the involved parties, overcoming common obstacles and speeding up the process, plus added extras including email templates to handle common roadblocks.

How long is the process of buying a house?

The speed of the process to buy property depends on a number of factors and a key factor is how many people are involved. If you are buying a freehold property then you’ll be working with your solicitor, seller’s solicitor, seller, estate agent and local council. If you are buying a leasehold property then you can add the freeholder, freeholder’s solicitor and managing agents. There are a lot of people in this loop and if one person goes on holiday, only sends by post or has a delay then everyone else is affected.

On top of all this, if you are in a chain of sales and purchases, the whole chain could be affected by one slow party in the chain. Organising all these people and getting everyone to work harmoniously is the job of your conveyancing solicitors so make sure you choose wisely.

How To Buy A House

Without Killing Anyone

Without Killing Anyone

This book could be the difference between every mover’s dream, buying and moving into your new home stress free, or, stress, missed deadlines, legal disasters, building defects, and possibly the collapse of the whole transaction. (Costing you a small fortune, a head full of grey hairs, and, driving you to threaten the life of your solicitor, lender, co-owners, family, partner, or some combination of all five).

With more than two decades’ experience in the conveyancing sector and over 50,000 successful client moves under his belt, Andrew shares insider tips and advice to empower you as a buyer, giving you the tools to make the best decisions for your circumstances and ease the chaos.

£9.99 (No VAT)

Available on Amazon | Kindle | Paperback

Available on Amazon | Kindle | Paperback

Acknowledgements

I cannot thank my editors enough. I’ve worked with them for years and I learn so much from their technical knowledge and client focused approach. I appreciate their input and their patience. Having two highly experienced solicitors editing this book means my insider guidance is backed, verified and cross examined with their technical expertise.

Plus, I am grateful to have also had an amazing writer editing this book, who fine tuned my words and picked at my loose threads, nudging me to weave them all together and round out this complete end to end guide.

Sarah Haller, Property Solicitor

Sarah is a Partner at Chadwick Lawrence Solicitors in West Yorkshire. She is Head of Conveyancing at her practice, in addition to being the firm’s Money Laundering Reporting Officer and Senior Responsible Officer for the Law Society’s Conveyancing Quality Scheme.

Sarah’s whole career in the legal profession has been at Chadwick Lawrence where she started as a temporary legal secretary 25 years ago. For most of her time at the firm she worked on client files but now, with a department of almost 80 people to keep in check (alongside her senior management team), she sticks to management, compliance, procedure, strategy, and external conveyancing relationships.

Caragh Bailey, Content Guru

Thanks also to my editor and proof-reader. Caragh is my senior copy writer of online content. She joined my company a few years ago, bringing her natural talent for writing.

She has contributed excellent articles and editorial pieces to my websites and specialises in Search Engine Optimisation and Strategy.

She has a keen eye for structure, grammar, and flow, and I appreciate all her help. Proof is in the pudding and this pudding would be a mess without Caragh’s attention to detail.

Luciana Ispani, Conveyancing Solicitor

Lucy qualified as a Solicitor in September 1997, and has since then worked in property. She started her career with residential property sales and purchases, and then took on plot sales for a large, well-known developer. Since then, she has worked in a few different firms carrying out a mixed role of both residential and commercial property work, with some development along the way.

She estimates to have helped over 10,000 people over the years and is most grateful for the wonderful experience she has had, especially being able to practice with a mixed caseload, the lovely people she has worked with, and those that have mentored her along the way. She now works for our panel solicitor.

Frequently Asked Questions

SOLICITOR

AFFORD

FASTER

NEED

QUALIFY

BAD-CREDIT