Joint Tenants vs Tenants in Common: Which is best for you?

Choosing how to own property with another person is a critical legal decision that dictates your financial security and inheritance rights. Whether you are buying as a married couple, with a partner, or as an investor, you must choose between becoming joint tenants or tenants in common.

This choice determines what happens to your share of the property if you die, how you divide the proceeds if you separate, and whether you can protect an unequal deposit. This guide compares both structures to help you finalise the best arrangement for your specific circumstances, and the implications of changing.

Buy as

Joint tenants, or

Tenants in Common

By Andrew Boast, CEO of SAM Conveyancing

Differences between joint tenants and tenants in common

The legal title is always held as joint tenants, but the equitable interest, also called the beneficial interest, can be held as joint tenants or tenants in common, and these are the differences.

Feature | Joint Tenants | Tenants In Common |

|---|---|---|

Feature Ownership | Joint Tenants You both own 100% of the property together. | Tenants In CommonEach person owns a specific share (e.g., 50%/50% or 70%/30%). |

Feature Survivorship | Joint Tenants Automatically passes to the other owner on death. | Tenants In CommonPasses to whoever is named in your Will or lines of intestacy. |

Feature Control | Joint Tenants Cannot assign your beneficial interest to anyone, including the other legal owner. | Tenants In CommonCan act independently regarding your specific share. |

Feature Better suited towards | Joint TenantsMarried couples protected by Family Law. | Tenants In CommonUnmarried couples, family, friends and investors. |

Change to Tenants in Common Today

- Whether for tax planning or divorce/separation.

- Deeds drafted within 2 working days(1).

- Applications made digitally to the Land Registry within 5 working days(2).

- Fixed Fee of £260 INC VAT for a deed and a severance, or £260 INC VAT for just the severance.

When do you choose the ownership?

You choose the ownership structure when you originally purchased the property together, or when you added them to the title. A Form TR1 is predominantly used for land transfer, and in section 10, you declare how you hold the beneficial interest.

Declaration of trust. The transferee is more than one person and:

- they are to hold the property on trust for themselves as joint tenants

- they are to hold the property on trust for themselves as tenants in common in equal shares

- they are to hold the property on trust...in unequal shares

The TR1 Form is a Land Registry deed and is written in stone, and is evidence of what the owners agreed to. This is why most owners get a deed of trust because they want to state more than just what the TR1 asks in Box 10.

Can you change your title ownership?

You can change from Joint Tenants to Tenants in common for free at any time you like; however, it is harder to change to joint tenants.

Does changing ownership trigger stamp duty?

No, you can change your ownership without triggering a stamp duty liability. You will only become liable for stamp duty if you transfer any of the beneficial interest between you. Here is a more detailed article on Stamp Duty on Transfer of Property Between Spouses.

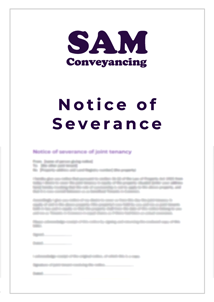

Download our notice of severance template in PDF or Word format, free from hassle.

- Instant download.

- Easy to fill in.

- Suitable format to submit your notice of severance.

The templates will be attached to your confirmation email after payment. Please allow a couple of minutes for the email to arrive.

What are the Pros & Cons of each type?

The pros and cons of each ownership structure vary depending on your circumstances and relationship. Whilst this is a guide, your relationship may suit a non-typical ownership.

The Pros and Cons of Beneficial Joint Tenancy | The Pros and Cons of Tenants in Common |

Pros

| Pros

|

Cons

| Cons

|

Decision Matrix: Married vs Unmarried vs Investors

The relationship of the joint owners dictates how you should own the property, and this is a breakdown of why and things you should consider.

Relationship of Owners | Recommended Ownership | Primary Reason | Key Requirement |

|---|---|---|---|

Relationship of Owners Married Couple | Recommended Ownership Joint Tenant | Primary Reason Simplifies inheritance via the Right of Survivorship; property passes automatically without probate. | Key Requirement A valid Will is still advised for the surviving partner. |

Relationship of Owners Un-Married Couple | Recommended Ownership Tenants in Common | Primary Reason Protects individual deposits and ensures assets pass to chosen heirs rather than automatically to a partner. | Key Requirement Deed of Trust to define shares and an exit strategy. |

Relationship of Owners Buy-to-Let Investors | Recommended Ownership Tenants in Common | Primary Reason Allows for unequal split of rental income for tax efficiency (via HMRC Form 17). | Key Requirement Deed of Trust to confirm beneficial interest for tax purposes. |

Relationship of Owners Friends/Family Buying Together | Recommended Ownership Tenants in Common | Primary Reason Ensures each party’s financial contribution is legally ring-fenced if the relationship changes. | Key Requirement Floating Deed of Trust if contributions to the mortgage change over time. |

Expert Tip - The top considerations for choosing your title ownership

- Inheritance: As joint tenants, you cannot leave your share of the property to anyone else in your Will; it always goes to the co-owner. As tenants in common, you have full control over who inherits your share.

- The "Exit Strategy": It is significantly easier to manage a separation or a "buy-out" as tenants in common because your specific financial stake is already documented.

- Legal Protections: If you are not married, the law provides very little "automatic" protection. Moving forward as tenants in common with a Deed of Trust is the most robust way to handle enquiries regarding your equity.

CEO of SAM Conveyancing

Frequently Asked Questions About Joint Tenants vs Tenants in Common

Andrew Boast FMAAT is a qualified accountant, conveyancing specialist and author with over 25 years of experience in the UK property sector. Since beginning his career in 2000 within established SRA and CLC-regulated conveyancing solicitor firms, Andrew has overseen the legal journeys of more than 75,000 clients.

He is the self-published author of the first-time buyer guide: How to Buy a House Without Killing Anyone, and a frequent contributor to mainstream UK media on legislative updates, property law, first-time buyer guides, conveyancing best practices, and stamp duty changes. Andrew specialises in resolving complex title issues, property conflict disputes, and property tax options, streamlining the enquiry process to reduce transaction times and maintaining a client-friendly focus.

Amanda Ambler is a highly accomplished conveyancing specialist with over 15 years of dedicated experience across residential property law, legal compliance, and practice management. Having held senior roles, including Head of Legal Practice and Head of Conveyancing at established UK law firms, Amanda possesses a profound, hands-on understanding of the technical intricacies of the property market.

As the designated Legal Content Reviewer for SAM Conveyancing, Amanda ensures that every guide, legal update, and resource published meets the absolute highest standards of accuracy, regulatory compliance, and factual integrity. Her rigorous review process guarantees that complex property legislation and industry processes are communicated clearly, transparently, and safely for home buyers and sellers alike.