![]()

What is the Capital Gains Tax on Gifted Property?

Capital gains tax on gifted property is payable depending on the relationship or connection between the owner of the property and the party/ies being gifted the property. If there is a connection or a relationship, the capital gains tax will be payable on the full market value.

HMRC will examine the relationship between the seller and the buyer to see how to treat the capital gains tax on gifts, especially if the property is being transferred under market value.

A remortgage will have CGT considerations on a transfer of beneficial interest as well as a legal ownership transfer.

You don't need to pay CGT if:

- You lived in the home the entire time (primary residence).

- You give it to your spouse.

- You put the property into a trust for the benefit of your child (CGT will be deferred until your child sells).

Capital Gains Tax on gift of property to child

The good news is that there is no Capital Gains Tax on your principal place of residence (where you live); there is only CGT on second properties (such as a buy-to-let or a holiday home).

The rules around the gift of property to children are set out here - CG14530 - Consideration for disposal: market value rule.

How can you gift a property to your child?

The most common way to transfer property under market value is often called a Concessionary Purchase.

We specialise in gifting property to children and completing the transaction quickly. Call us for questions, or click the button below to get a Fixed Legal Fee Quote.

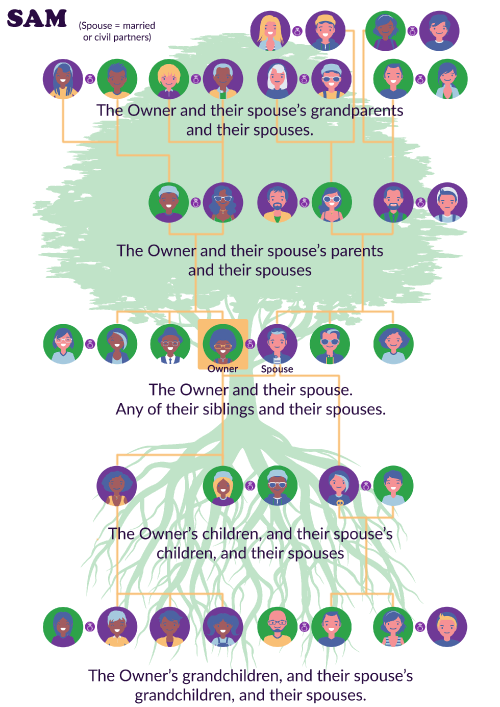

Connected person CGT - a family tree

When a property is gifted to a connected person, the donor will be liable for Capital Gains Tax on the full capital gain, based on the current market value regardless of whether any money was paid for it.

If a donor incurs a capital loss from a gift, this loss cannot be used to offset other capital gains unless the recipient later sells the asset at a profit.

Example:

If you gift a property worth £500,000 to your child (a connected person), and your original purchase price was £200,000, you will be liable for CGT on the £300,000 gain. Even though you haven't sold the property, the gift to your child is treated as a sale at the market value of £500,000.

Your child will then own the property with a base cost of £500,000 (the market value at the time of the gift). If they later sell the property for more than £500,000, they will have to pay CGT on the difference.

Below is an example of a family tree, showing people who are connected to the owner for CGT purposes.

How do you calculate Capital Gains Tax on property?

| | £ |

| Proceeds from the sale of the property at Market Value | i.e £500,000 |

| Take Away | |

| Costs of disposal - eg. estate agent's fee, solicitor's fee , extension/improvement costs | i.e £25,750 |

| Equals = net proceeds of the sale | i.e £474,250 |

| Take Away | |

| Original purchase price of property | i.e £200,000 |

| Costs of original purchase - eg. stamp duty, Land Registry fees, solicitor's fee | i.e £1,500 |

| Gain (or loss) | i.e £272,750 |

| Capital Gains Tax allowance - the annual exemption | (2024-25) £3,000 |

| Amount subject to Capital Gains Tax | i.e £269,750 |

You should speak to a tax advisor for capital gains tax advice.

What is the rate for Capital Gains Tax on gifted property?

| Tax Band | Income Tax Band | Capital Gains Tax Rate (chargeable on profits) |

| Basic rate income tax payer | £0 to £50,270 | 18% |

| Higher rate income tax payer | Over £50,271 | 24% (post 6th March 2024 budget) |

- Fixed Fee Conveyancing from £399 INC VAT.

- Services including Help to Buy, Shared Ownership, joint owner disputes, or simply adding a new name to the title.

- Fast Completions and Efficient Transfers.

- On 99% of mortgage lender panels.

- Friendly and helpful specialists in transfer of equity transactions.

Andrew Boast FMAAT is a qualified accountant, conveyancing specialist and author with over 25 years of experience in the UK property sector. Since beginning his career in 2000 within established SRA and CLC-regulated conveyancing solicitor firms, Andrew has overseen the legal journeys of more than 75,000 clients.

He is the self-published author of the first-time buyer guide: How to Buy a House Without Killing Anyone, and a frequent contributor to mainstream UK media on legislative updates, property law, first-time buyer guides, conveyancing best practices, and stamp duty changes. Andrew specialises in resolving complex title issues, property conflict disputes, and property tax options, streamlining the enquiry process to reduce transaction times and maintaining a client-friendly focus.

Amanda Ambler is a highly accomplished conveyancing specialist with over 15 years of dedicated experience across residential property law, legal compliance, and practice management. Having held senior roles, including Head of Legal Practice and Head of Conveyancing at established UK law firms, Amanda possesses a profound, hands-on understanding of the technical intricacies of the property market.

As the designated Legal Content Reviewer for SAM Conveyancing, Amanda ensures that every guide, legal update, and resource published meets the absolute highest standards of accuracy, regulatory compliance, and factual integrity. Her rigorous review process guarantees that complex property legislation and industry processes are communicated clearly, transparently, and safely for home buyers and sellers alike.