![]()

Gifted Deposit Process Explained

With the average price of a property in England and Wales reaching £286,768 (Dec 2025) , the average 15% deposit first-time buyers spend of £43,015 (Dec 2025) is unachievable without help. The ONS English Housing Survey reports that gifted deposits are used in 37% of first-time buyer purchases, and most commonly, the deposit needed to buy a house comes from the bank of Mum and Dad.

While the gift doesn't always have to be from your parents, you may find that some mortgage lenders won't allow a gift from siblings. There are also Builder Gifted Deposit incentive schemes, in which developers offer first-time buyers a portion of their deposit.

The gifted deposit process is detailed below. We explain how to pay a cash gift, how much you can gift, who can make a gift of a deposit, mortgage lender complications, and any tax implications.

a solicitor

need for a

Gifted Deposit?

By Andrew Boast, CEO of SAM Conveyancing

What is a gifted deposit?

A gifted deposit is money paid by a third party to a buyer to help them purchase a property. The gift is either part or all of the deposit, reducing the mortgage needed to an affordable level for the buyer.

How does this work?

Even if you can afford the minimum deposit on your own, by paying a higher ratio of the property's value in the deposit, you need to borrow less, making your monthly payments and total repayment more affordable for two reasons:

- The total loan amount is smaller; you pay interest as a percentage of the total loan amount, so your interest payments will be lower.

- You may qualify for a lower rate of interest: the greater the deposit ratio, the lower the loan risk is deemed by lenders, meaning you can access a wider choice of mortgage products, which are often at better interest rates. This means you'll pay interest at a lower percentage of the total loan amount.

This works best if the gift is truly a gift, with no expectation of repayment. The giver has no legal or beneficial rights over the property or any proceeds from rental income or sale. If the 'gift' is really a loan, the lender will usually treat it as a liability.

Can I protect the gift from going to their partner?

Yes, we can protect the gift amount using a Deed of Trust, which can show that the amount is returned to your child. If married to their joint owner, this may be overruled by a family court.

The buyer's solicitor must formalise the gift, ensuring that the person providing the gift meets the mortgage lender's guidelines; you can't simply gift money to buy a property in England and Wales.

What is the gifted deposit process in 3 steps?

The buyer's solicitor follows a particular process when there is a gift for the buyer, but mainly on behalf of the mortgage lender. This is what any conveyancing solicitor in England and Wales will need if you are using a gifted deposit:

- 1

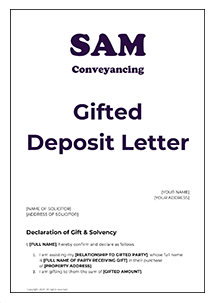

Deposit Gift Letter

A gifted deposit letter is a legal document that needs to be completed by the person providing the gift. If the deposit gift is from your parents, grandparents, or siblings, they must fill in this letter confirming it is a gift, that they have no right to request the money back, have no claim to the property, and are solvent.

The letter is a deed and will need to be signed and witnessed, and posted back to the buyer's conveyancing solicitor. Read more - What is a Gifted Deposit Letter?

Download a gifted deposit letter template, free from hassle.

- Instant download

- Easy to fill in

- Suitable for mortgage lenders

- Sign, witness and gift the money

The templates will be attached to your confirmation email after payment. Please allow a couple of minutes for the email to arrive.

£4.99 INC VAT

Some mortgage lenders have specific gifted deposit templates, such as Nationwide - Source of Deposit.

- 2

Proof of Identification

The solicitor must know the identity of anyone providing money to purchase the property to adhere to money laundering regulations, including any money gifted, now or in the past. The person providing the gift must provide the following:

Photo ID | Proof of where you live (a minimum of 2 are required) |

|

|

We offer identification checks for our gifting mums and dads via an online portal for speed and ease. You can instantly load your ID into our App and avoid lost personal documents. You should ask your solicitor if they offer a similar service.

- 3

Source of Funds

Another part of the Anti-Money Laundering checks the buyer's solicitor must undertake is to confirm the source of the gift. For most, it’ll be from a sale of an expensive asset (normally a house), a pension drawdown or the sale of shares; all of these are easy to prove with copies of the relevant documents showing where the large sum of money has come from and a download of your bank statement where the money is held; normally 6 months worth of statements, but it can be as long as 1 year. Actual cash gifts cannot be used as you cannot verify their source.

What is harder to prove is when funds have been accrued from earnings over a long period, come from multiple sources, or come from overseas. Both sources must be explained in detail to satisfy the solicitor and meet their AML procedures. Once again, these procedures vary considerably from solicitors to solicitors, however most should be satisfied if you can properly evidence where the money has come from. For more complex scenarios, read more - How do I prove where my gift deposit came from? and How do I prove gifts from overseas?

There are also new online sources of funds checkers such as Armalytix to help solicitors compliance check the financial statements provided. Online software such as this can reduce the volume of manual statements provided by the gifter and offer the solicitor greater assurance.

What are the complications with the mortgage lender?

When buying a house with a gifted deposit, you must inform your mortgage lender; not all allow a gift. Some buyers choose not to do this at the outset as they already have the money in their bank account. This isn't a good idea, as the gift will come to light later, and it'll delay the mortgage application process.

Getting a gift is so common now, so it is ok to declare it from the outset. What the mortgage lender will want to know, though, is that it is a gift and not a loan. Read more about the Complications of a Gifted Deposit Mortgage.

Who can gift a deposit?

The Bank of Mum and Dad mortgage deposits are the most common gifts; almost all high street lenders will allow this. Similarly, a gift from your Nan and Grandad would be fine. You may struggle if the gift comes from siblings or friends. The reason is that, unlike a gift deposit from your parents, a sibling or friend is likely to expect to have the money returned. Some mortgage lenders allow gifts from siblings/friends, so ask your mortgage lender/broker early in your mortgage application if you are getting a loan from either.

Parents gift £13,000 more to sons buying their first home

Zoopla reported that the Bank of Mum and Dad gifted an average of £58,000 to fund their children's first home purchase. This reduced the average age to get onto the property ladder from 39 to 33.

There was, however, a difference in the sums gifted between the child's gender, with sons receiving an average of £65,000 and daughters £52,000. Source: Zoopla.

What tax do I pay on a gifted deposit?

The buyer doesn't pay any tax on the gift they receive. Anyone can gift you any money, and the person receiving the gift won't have to pay tax. It isn't income from work or a gain on the sale of an asset; it is just a gift.

The gifter, on the other hand, may have to. While a gift doesn't attract income or capital gains tax, it could fall under inheritance tax. You have a tax-free allowance of £3,000 per year for gifts. Any gift after this would fall under Inheritance tax under the 7-year rule for gifts.

| Number of years before death | Rate of IHT on the gift |

| 0 to 3 Years | 40% |

| 3 to 4 years | 32% |

| 4 to 5 years | 24% |

| 5 to 6 years | 16% |

| 6 to 7 years | 8% |

| 7 or more years | 0% |

Do all gifts need to be declared?

A common question asked by SAM Conveyancing clients, and the answer is yes, they do. The buyer's solicitor needs evidence of the source of all the money being used to fund the purchase, no matter how small it is. In reality, receiving small gifts of £1 from your parents would be weird by bank transfer. More common would be when they pay you larger sums of money for your house deposit.

Can the gift be repaid like a loan?

In the past, mortgage lenders were more strict on gifts that would be repaid; however, some mortgage lenders allow this. These lenders will expect the gifter to declare the gift; however, it is agreed that the gift will be repayable upon the sale of the property. This means that although it isn't a loan, which has interest and could be called upon to be repaid before the sale, it'll be a gift that gets repaid on sale only.

This type of gift is good for the buyer as they get to buy using a higher mortgage deposit, but it could be a risk for the gifter as they can only get the money back from the sale. If the buyer refuses to sell, this money could remain with the buyer.

What are the Builders Gifted Deposit schemes?

Some new-build developers offer incentives for first-time buyers to pay their deposit. In most cases, this is a reduction in the actual asking price of the property and not an actual paid cash incentive. The buyer will still need a gifted deposit mortgage of 95%/100% of the property's price. Read more: How to buy a house with a 5% deposit?

What if you can't afford a gifted deposit?

It may not always be that your parents can afford to gift you the deposit you need to buy your first home. This doesn't mean they can't help, as many mortgage products are in the market to help first-time buyers onto the property ladder. For example:

Joint Mortgage Sole Proprietor

With this mortgage product, your mum and dad could go on the mortgage application with you and help reduce the size of the deposit you need by having a larger mortgage affordability. Your parents would be named on the mortgage alongside you, but you'd be 100% the legal owner of the property. You get the benefit of their financial backing but still buy your own home.

There are risks to consider when looking at this specific type of mortgage, which we have set out here: a joint borrower sole proprietor mortgage.

95% mortgage guarantee Scheme

The Government has launched a New 95% mortgage scheme that allows you to have a smaller deposit of just 5%. Many high-street mortgage lenders offer this scheme, including Barclays, Lloyds, HSBC, and Halifax.

37% of First-time buyers receive a gifted deposit

The Office for National Statistics released the English Housing Survey figures. Within the report, they monitor the source of deposits for first-time buyers. In 2022-23, 37% of first-time buyers used a gift to fund their mortgage deposit in part or in full. This is an increase on the previous year of 35%.

about a

Gifted Deposit

By Andrew Boast, CEO of SAM Conveyancing

Andrew Boast FMAAT is a qualified accountant, conveyancing specialist and author with over 25 years of experience in the UK property sector. Since beginning his career in 2000 within established SRA and CLC-regulated conveyancing solicitor firms, Andrew has overseen the legal journeys of more than 75,000 clients.

He is the self-published author of the first-time buyer guide: How to Buy a House Without Killing Anyone, and a frequent contributor to mainstream UK media on legislative updates, property law, first-time buyer guides, conveyancing best practices, and stamp duty changes. Andrew specialises in resolving complex title issues, property conflict disputes, and property tax options, streamlining the enquiry process to reduce transaction times and maintaining a client-friendly focus.

Amanda Ambler is a highly accomplished conveyancing specialist with over 15 years of dedicated experience across residential property law, legal compliance, and practice management. Having held senior roles, including Head of Legal Practice and Head of Conveyancing at established UK law firms, Amanda possesses a profound, hands-on understanding of the technical intricacies of the property market.

As the designated Legal Content Reviewer for SAM Conveyancing, Amanda ensures that every guide, legal update, and resource published meets the absolute highest standards of accuracy, regulatory compliance, and factual integrity. Her rigorous review process guarantees that complex property legislation and industry processes are communicated clearly, transparently, and safely for home buyers and sellers alike.